If you file for bankruptcy, it is natural to worry about your ability and credit score. While it is normal to want to open new credit lines, it is important to repay your existing debts on time. This is why programs for bankruptcy counseling should provide information about budgeting and debt relief. You may also find guidance through nonprofit credit counseling agencies such the National Foundation for Credit Counseling.

Timely payment of bills

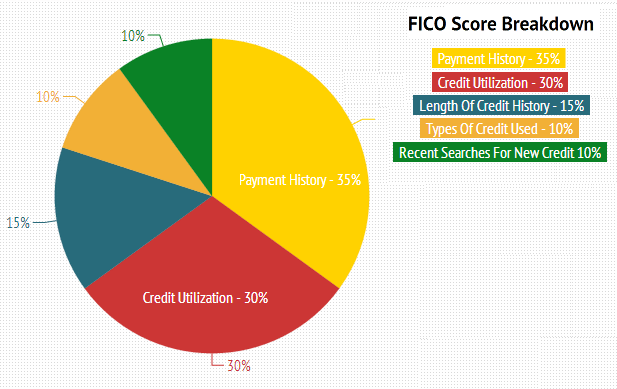

Payments on time are a crucial aspect of credit restoration after bankruptcy. Paying your bills on time is crucial to rebuild your credit. Your payment history accounts for 35% of your FICO Score. It is also a smart idea to limit your monthly costs. It will help you keep track of your expenses and stop the debt cycle.

It is a great way to rebuild your credit score after bankruptcy. Start by paying off any outstanding bills. After your debt has been paid, you can start to create an emergency fund. Spend less than you earn, so it is essential to have money saved for unexpected expenses.

Use secured credit cards

Secured credit cards are one of the best options to rebuild credit following bankruptcy. These cards require a minimum deposit of at least the card's credit limit. This deposit cannot be refunded unless you close the card or upgrade it. These cards can help improve your credit score and establish a strong credit record.

Because the credit limit is limited to the amount of the security deposit, this card is easy to get after bankruptcy. Unsecured card cards, on contrast, do not check your credit rating and may even allow you to get credit after bankruptcy. These cards have a downside: high fees and exorbitant interest rates.

Using Peer to Peer loans

Lenders can be suspicious of bankruptcy filings. This is because their previous loans have been either liquidated completely or partially, so they are suffering a financial loss. There are some steps you can take to rebuild your credit following bankruptcy. You should first be open about your situation and show proof of your financial management. You must also show proof that you have made savings.

A clean credit report is an essential step in rebuilding credit following bankruptcy. You can get a copy of your credit report from the three major bureaus for free. You can then take steps to correct any errors.

Negative information about your credit report is able to be corrected

While bankruptcy can cause damage to your credit history it is possible to rebuild it. There are many steps you can take to restore your credit immediately after filing for bankruptcy, including signing up for a free credit report and score. Even if credit isn't good, it can be rebuilt in just a few weeks.

You can start by writing to credit agencies to dispute inaccurate information. Under the Fair Credit Reporting Act, the bureaus are obligated to investigate disputes and remove inaccuracies. A note explaining your side can be written and will appear on any future credit reports. You will have the information for seven years. Therefore, it's crucial to act now.

Applying to a new credit-card

It's possible to get a new credit card to rebuild your credit after bankruptcy. Although credit card companies have to report your payment activity to the credit bureaus, a low utilization rate can help you rebuild your credit faster. It's best not to have any balance and to pay it immediately.

If you want to rebuild your credit following bankruptcy, lenders will need to see that you are responsible with your money. Your credit score will be largely affected by your credit card payment history. Therefore, it is important to manage credit cards responsibly. Although credit cards are available to help you pay for purchases that you can make immediately, you should be careful not to overextend your budget and get charged high APRs.