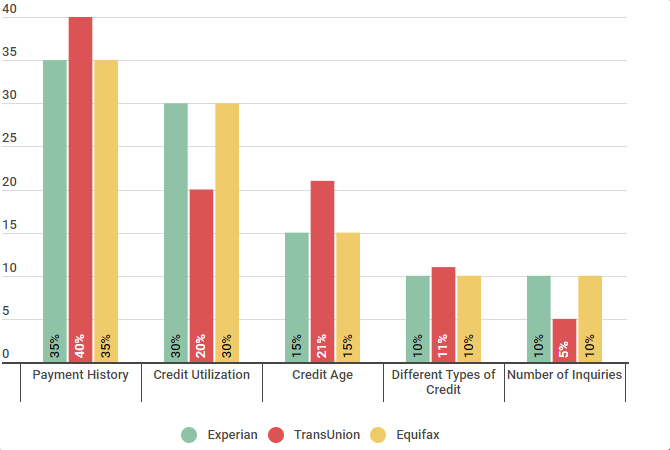

You're not the only one wondering about what the difference is between having a high credit score and one that's low. According to experts, the question of what is bad credit score really depends on what you're looking to use your credit for. Your credit score is determined by five major categories: credit mix, payment history, amount due, length of credit history, new credits, and payment history. Each category contributes a percentage to your overall score.

A bad credit score can have negative consequences

A bad credit rating can negatively impact your life in many ways. First of all, it will make it more difficult to get loans or to receive credit from lenders, and you'll be required to pay higher interest rates. It will be more difficult to find work or rent an apartment if you have a low credit score. You will also have a harder time getting a car loan and may have difficulty getting utilities set up. A higher rate of auto insurance and higher rates in some states for health insurance will make it more difficult to get a car loan. Potential employers will notice a poor credit rating.

There are several ways to increase your credit score. First, you should refrain from opening new credit accounts. Although it is not a good idea to open new lines credit, it is important you maintain a balance between different types of credit. Keeping your credit mix diverse will show lenders that you can manage your finances.

You can improve your credit score by following these steps

One of the best ways you can improve your credit score, is to make sure that you keep up with your payments. You can damage your credit score by missing a single payment. There are many things you can do in order to keep your payments on track. You credit score can be affected by several factors such as your payment history, credit utilization, and debt.

Your credit score will improve if your balances are less than 10% of your available credit. But, remember that exceeding your credit limit could lower your credit score. You should try to pay off your debt whenever possible instead of transferring it to another card. This is a great way to improve your credit score, even though it may seem counterintuitive.

It is a good idea to not open any new credit accounts. Opening new accounts can result in a hard inquiry on your report, which will lower your score. Furthermore, opening new lines credit can decrease the length and importance of your credit history.

Bad credit is not a problem when you apply for a consolidation loan.

Poor credit scores can make it difficult for you to qualify for a consolidation loan. There are several ways to improve the credit score. Within six to twelve month, you will start to notice improvements in your credit score. If you have poor credit, bankruptcy might be an option. But it should not be your last resort. A professional credit counselor will help you decide whether bankruptcy is the best option for you.

There are many types of debt consolidation loans you can apply to. The credit score requirement will vary between lenders. Most lenders require that your FICO be at least 600. Some will even accept scores as low at 580. You must monitor your score to make sure you're eligible for the best loan. Many banks and online tools make it easy to check your score.